Solve Trust, Own the Decade: The Case for Agentic Finance

Every decade or so, financial infrastructure undergoes a phase transition. Not an incremental improvement, a genuine change in the underlying physics of money. The magnetic stripe card in 1969. The Automated Clearing House (ACH) network in 1974. PayPal normalising internet payments in 1999. Stripe making payments a developer primitive in 2010.

We are at such a moment again. And the industry is not ready.

AI-enabled autonomous agents are beginning to interact with the global payments market - which processed approximately $1.8 quadrillion in transaction value in 2023 - not as tools, but as principals. They initiate transactions. They route payments. They settle obligations. They do this without moment-to-moment human instruction. Gartner estimates that by 2028, AI agents will autonomously handle 15% of day-to-day financial decisions for early-adopter consumers. That is not a rounding error. That is a structural shift in who - or what - controls the allocation of capital.

The next Google, PayPal, or Stripe is most likely to emerge from the agentic payments stack. The disruption is not confined to a single vertical. It is, theoretically, the total addressable supply of money. But the sector faces three structural deficits that, if left unresolved, will either delay adoption by a generation or produce the kind of catastrophic consumer harm that invites blunt regulatory action, and possibly overreaction. Those deficits are: the absence of standards, legislation written for a different century, and - most critically - a profound trust deficit.

The Standards Problem

The internet nearly failed in the 1990s for precisely this reason. Before HTTP, HTML, and TCP/IP became de facto standards, the commercialisation of the web was held hostage to incompatible proprietary protocols. The browser wars were not primarily about features - they were about who would set the standards that determined interoperability. The W3C, founded in 1994, ultimately provided the governance structure that unlocked the commercial internet.

Agentic payments have no comparable body. There is no agreed schema for how an agent should authenticate itself to a merchant. No standard for expressing a user's spending mandate. No common format for conveying transaction provenance - the chain of delegation from human principal to AI agent to payment network. Without these, every implementation is bespoke, every integration is fragile, and the market will morph into walled gardens that harm consumers and smaller merchants most.

Some of the most promising early work is happening at the infrastructure layer. At Sumvin, we have built our platform around a cryptographically anchored, portable credential that allows AI agents to prove both who they represent and what they are authorised to do - across platforms and services, without repeated onboarding or fragmented identity checks. Built on Sei Network, I believe Sumvin is the kind of primitive the industry needs: not proprietary, not fragile, but verifiable by design. The most plausible path to broader standardisation is a hybrid governance model: an industry consortium - comparable to EMVCo, which governs chip-and-PIN standards globally - operating under the oversight of a formal standards body such as ISO or ANSI. The specifications required are not technically complex. They are politically complex, because they determine whose infrastructure sits at the centre of the new stack. That political difficulty is not a reason to delay. It is precisely the reason to start now.

Legislation Written for Yellow Cabs

Consumer protection law, in virtually every major jurisdiction, was architected around a foundational assumption: that a human being is always, at some meaningful point in the transaction chain, in the loop. The Electronic Fund Transfer Act of 1978, PSD2, the UK's Consumer Rights Act of 2015 - all presuppose a model of financial agency that is fundamentally incompatible with fully autonomous AI-initiated transactions.

Consider the concept of an 'unauthorised transaction.' It becomes philosophically unstable when the entity initiating the transaction is an agent that was authorised to act - just not, perhaps, to make this specific decision in this specific context. The US Consumer Financial Protection Bureau’s 2023 inquiry into AI in financial services acknowledged this gap without closing it. The EU AI Act, which came into force in August 2024, establishes risk categories for AI systems but contains no provisions specific to financial agency or agentic payment flows.

We are, in regulatory terms, in the equivalent of the early days of ridesharing - a genuinely novel economic activity being conducted under legal frameworks designed for yellow cabs. The industry's response to this should not be to lobby against regulation. It should be to participate actively in its design: to provide regulators with a conceptual vocabulary that allows them to differentiate between low-risk recurrent payments and high-value autonomous advisory functions. Undifferentiated regulation - treating all agentic payments as equivalently risky - would be both economically destructive and technically illiterate.

Trust Is a Technology

This is the most important problem, and the one most amenable to design. I don’t think trust should be seen as a sentiment. It is a technology, and, like all technologies, it must be deliberately engineered.

Consider commercial aviation. Modern fly-by-wire aircraft can execute an entire flight with minimal pilot intervention. The FAA reports that human error remains a factor in approximately 75–80% of aviation accidents, which means automation has, empirically, made flying dramatically safer. Public trust in aviation was not built through transparency into avionics code. It was built through an elaborate sociotechnical system: rigorous certification, incident reporting frameworks, clear accountability structures, and a visible human in the cockpit who consumers understand is there to catch edge cases.

Waymo is instructive for a different reason. Its public deployment has proceeded not because the technology is infallible - it is not - but because Waymo invested heavily in what trust researchers call 'legibility': the capacity of a system to communicate what it is doing and why. The car signals its intentions. It stops predictably. It satisfies the need for process transparency even when outcome transparency - explaining every algorithmic decision - is impossible.

The stakes in agentic payments are, by any rational measure, lower than in aviation or autonomous vehicles. A miscalibrated spending agent buys too many pairs of shoes. A miscalibrated autopilot kills people. And yet the financial services industry has consistently underestimated the asymmetry of consumer trust - the oft cited Warren Buffett insight that trust takes years to build and seconds to destroy. The design challenge for agentic payments is not to prevent all errors. It is to make errors recoverable, legible, and to ensure the baseline level of consumer benefit is compelling enough to sustain confidence through the inevitable early failures. This is the design philosophy behind Sumvin. Rather than asking users to hand over open-ended access to their finances, the platform is built around permissioned, bounded autonomy: users set goals, preferences, and limits; the system executes only within those parameters. The credential layer makes every action attributable and auditable.

A Framework for Sequencing Deployment

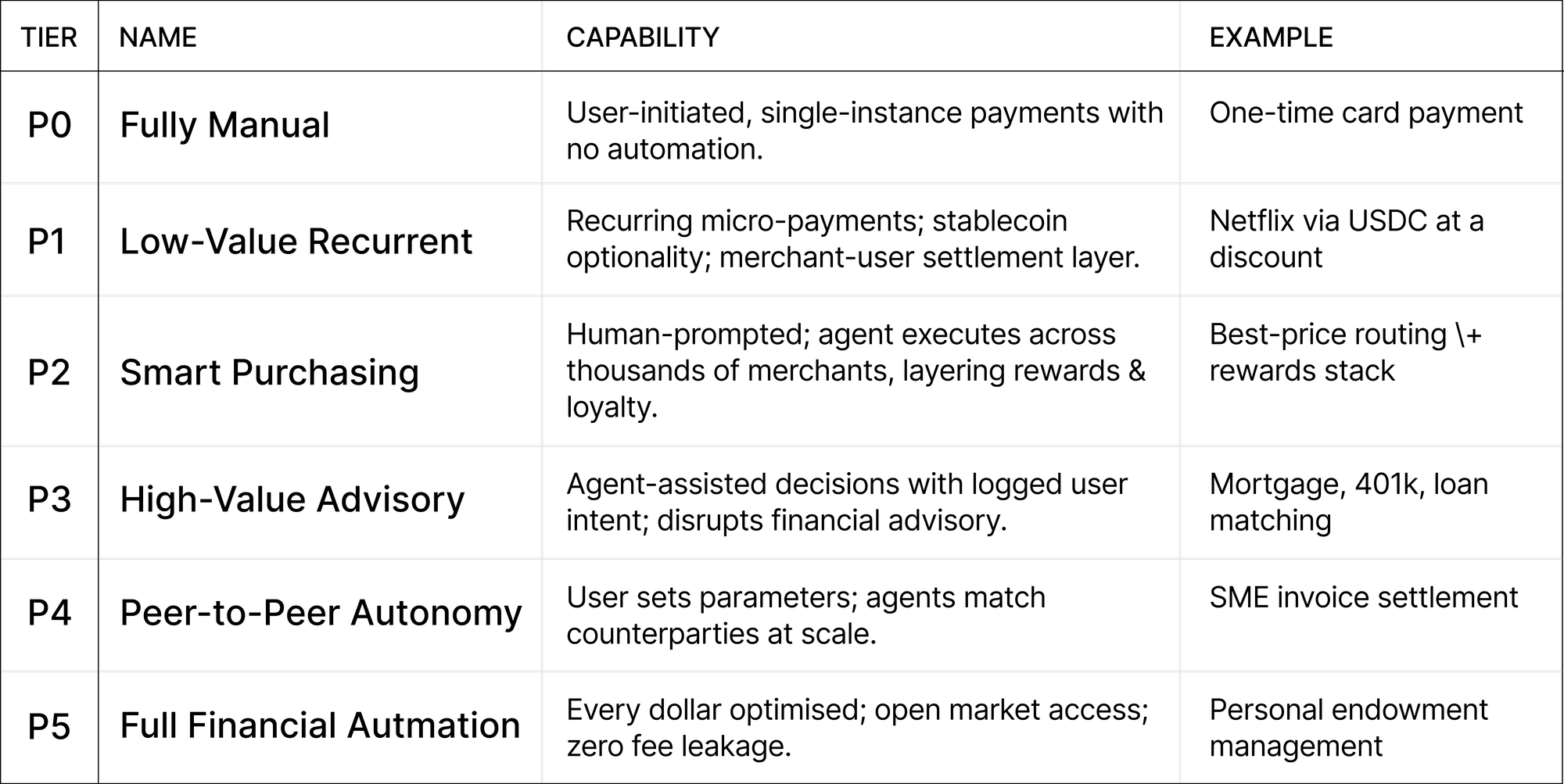

In my view, the industry needs a shared vocabulary for how agentic finance should be sequenced. Borrowing from the SAE International's autonomous vehicle classification system - which proved useful precisely because it gave regulators, engineers, and consumers a common language - I propose a six-tier Autonomy Stack for agentic payments:

P0 - Fully Manual. Single-instance, human-initiated payments. The baseline.

P1 - Low-Value Recurrent. The practical beachhead for agentic payments is recurring, low-value, predictable transactions. The Netflix monthly subscription is the paradigmatic example - not because the use case is exciting, but because it is low-risk, high-frequency, and thus highly amenable to the kind of A/B testing and behavioural analysis that generates the data required to build trust models. The meaningful innovation at this tier is the introduction of stablecoin optionality and merchant-user settlement negotiation. Consider the implications: Apple and Google currently extract a 30% commission on in-app transactions - a tax that is passed, in whole or in part, to consumers. A P1 agent capable of settling subscriptions via USDC on a stablecoin rail, bypassing the App Store entirely where legally permissible, could deliver material savings to consumers while simultaneously accelerating stablecoin adoption. The EU's Markets in Crypto-Assets regulation (MiCA), fully effective December 2024, provides the first comprehensive regulatory framework for stablecoin use in payments - a structural enabler that the market has not yet fully priced.

P2 - Smart Purchasing. Human-prompted; agent executes. This is where agentic payments begin to deliver capabilities that are genuinely superhuman - not in the sense of artificial general intelligence, but in the more prosaic and immediately valuable sense of doing things humans simply cannot do at scale. No individual consumer can simultaneously compare prices across thousands of merchants, apply loyalty point optimisation across multiple programmes, identify cashback opportunities, and route payment via the optimal instrument for a given transaction - all in under 200 milliseconds. An agent can. The key design principle at P2 is the primacy of human intent: the user provides the goal ('buy me the best-value running shoes in size 10'), and the agent handles execution. This 'intent-to-execution' architecture is not merely convenient - it represents a fundamental shift in consumer behaviour analogous to the shift from manually searching airline websites to using Kayak or Google Flights. The consumer moves up the value chain; the commoditised execution layer moves to software.

P3 - High-Value Advisory. This tier represents the most significant structural disruption to incumbents. The financial advisory industry manages approximately $114 trillion in global assets under management (Statista, 2024) and charges fees that, in aggregate, extract hundreds of billions of dollars annually from consumers - fees that are, in many cases, not correlated with outcomes. A P3 agent capable of conducting mortgage market analysis across every available lender, optimising 401k allocations against a user's stated risk parameters, or identifying the optimal loan structure for a small business owner is not a robo-advisor in the 2015 sense of that term. It is a wholesale replacement of the advisory function for the mass market - what venture capitalists call 'Wall Street to Main Street.'

The design constraint at P3 is accountability: there must be a logged, auditable record that the user intended to undertake the financial action in question. This is not merely a regulatory requirement - it is the mechanism by which trust is established and maintained. In aviation terms, P3 is the equivalent of the captain signing the flight plan: the human is not flying the aircraft, but their intent and authorisation is formally recorded.

P4 - Peer-to-Peer Autonomy. Agent-to-agent marketplaces. P4 introduces a qualitative shift: rather than executing against a fixed menu of merchant or institutional counterparties, the agent becomes a participant in a dynamic, agent-to-agent marketplace. The user establishes parameters - price limits, counterparty quality thresholds, settlement preferences - and the agent seeks matching counterparties autonomously. The SME use case is particularly compelling: a small business owner who today spends 4-6 hours per week on accounts payable and receivable (Intuit QuickBooks SME Survey, 2023) could instead define their treasury objectives and allow their agent to optimise continuously. This is not science fiction - it is a direct extension of the algorithmic market-making infrastructure that has operated in institutional equity markets for over two decades.

P5 - Full Financial Automation. P5 is the endgame: every dollar optimised, market access fully democratised, and the structural advantages currently available only to institutional investors - continuous portfolio rebalancing, tax-loss harvesting, cross-asset optimisation, real-time risk management - made available to every individual with a smartphone. The philosophical significance of P5 should not be understated. Access to sophisticated financial management has historically been a function of wealth: the more capital you have, the better the advisors you can access, which compounds into yet more capital. P5 dissolves this barrier. It is, in the precise sense of the term, a democratisation of financial infrastructure.

Getting to P5 requires two things: robust legislation (which will lag technology, as it always does) and a demonstrated track record of trustworthy performance at P1 through P4. This is not a counsel of despair - it is a sequencing strategy. The aviation industry did not begin with fully autonomous commercial flight. It began with autopilot-assisted cruise at altitude, built the regulatory and technical infrastructure iteratively, and expanded the envelope of automation as confidence accumulated.

What Must Be Built, and in What Order

Three parallel tracks of work are required, and they must proceed simultaneously rather than sequentially.

First, standards. The payments industry needs an analogue to the W3C - a multi-stakeholder body capable of producing and maintaining open specifications for agent identity, mandate expression, and transaction provenance. The most plausible governance model is a hybrid: an industry consortium (comparable to the EMVCo structure that governs chip-and-PIN standards globally) operating under the oversight of a formal standards body such as ISO or ANSI. The specifications required are not technically complex - they are politically complex, because they determine whose infrastructure sits at the centre of the new stack.

Second, legislative engagement. The regulatory gap will not close itself. The most productive posture for industry participants is not to lobby against oversight - it is to help design it. That means bringing regulators the conceptual vocabulary of the P0–P5 framework, or something like it, that allows them to differentiate between low-risk recurrent payments and high-value autonomous advisory functions. Undifferentiated regulation - treating all agentic payments as equivalently risky - would be both economically destructive and technically illiterate. The industry's job is to make differentiated regulation intellectually possible.

Third, and most importantly, trust infrastructure. This is where competitive advantage will actually be built. The companies that win in agentic payments will not be those with the most capable models - model capability will commoditise. They will be the companies that build the most legible, recoverable, and demonstrably aligned agent systems. That means investment in explainability interfaces (users should be able to see, in plain language, what their agent did and why), robust error recovery, and what might be called 'trust accounting' - a running record of agent performance that gives users the empirical basis for expanding or contracting their agent's autonomy over time. It is a design principle, not a feature. Most of today's financial tools are built on attention: they maximise engagement, surface notifications, and optimise for time spent in-app. Sumvin is building something categorically different - a platform that succeeds when the user does not have to think about it. That shift, from attention-based to outcome-based finance, is perhaps the deepest disruption in the entire agentic payments thesis.

The Plane Is Already Flying

There is a tendency in discussions of emerging technology to treat adoption as a future event - something that will happen once the technology matures, once regulators catch up, once consumers are ready. In agentic payments, this framing is already anachronistic. Agents are transacting. The question is not whether to build the infrastructure of trust. It is whether we build it deliberately and in advance, or reactively and after the first serious incident.

Flying is, by every objective measure, the safest form of long-distance travel ever devised. This did not happen by accident, and it did not happen because the technology was intrinsically safe. It happened because engineers, regulators, airlines, and consumers made a collective decision to invest in the systems, standards, and accountability structures that made safety computable and improvable. The result is a mode of transport in which humans board aluminium tubes, allow a computer to fly them at 35,000 feet, and don't think about it at all.

That is what trust infrastructure looks like when it works. That is what we are building now.

The opportunity in agentic payments is not merely commercial - though it is that too, massively so. It is the opportunity to rebuild the relationship between individuals and their capital on terms that are, for the first time, genuinely favourable to the individual. Every dollar optimised. Every fee eliminated that should be eliminated. Every market opened that was previously closed by the transaction cost of expertise. This is pure capitalism operating as it was theoretically intended to operate: efficiently, without unnecessary intermediation, in service of the individual who owns the capital.

The next PayPal will come from this space. So will the next financial scandal, if we are not careful. The difference between those two outcomes is the quality of the work we do in the next three years. The framework exists. The precedents exist. The only question is execution.