At the Network Effect Frontier

There's a moment in every empire's history when the very thing that made it great becomes the seed of its downfall. For consumer finance, that moment is now, and that thing is network effects.

Consider its elegance: every user makes a platform more valuable, which attracts more users, creating a perpetual motion machine of growth. It’s been the story of every fintech darling of the last decade.

But empires are surprisingly fragile things.

The irony is delicious: network effects succeeded too well. They created perfect walled gardens – not just for users, but for innovation itself. So it is high time they evolve.

What comes next transcends network effects entirely. The future belongs not to those who aggregate the most users behind the highest walls, but to those who can orchestrate value across a thousand different gardens, making the walls themselves obsolete.

The Rhymes of Aggregation

Barksdale's old adage – "there are only two ways I know to make money in business: bundling and unbundling" – has continued to hold true for over four decades now.

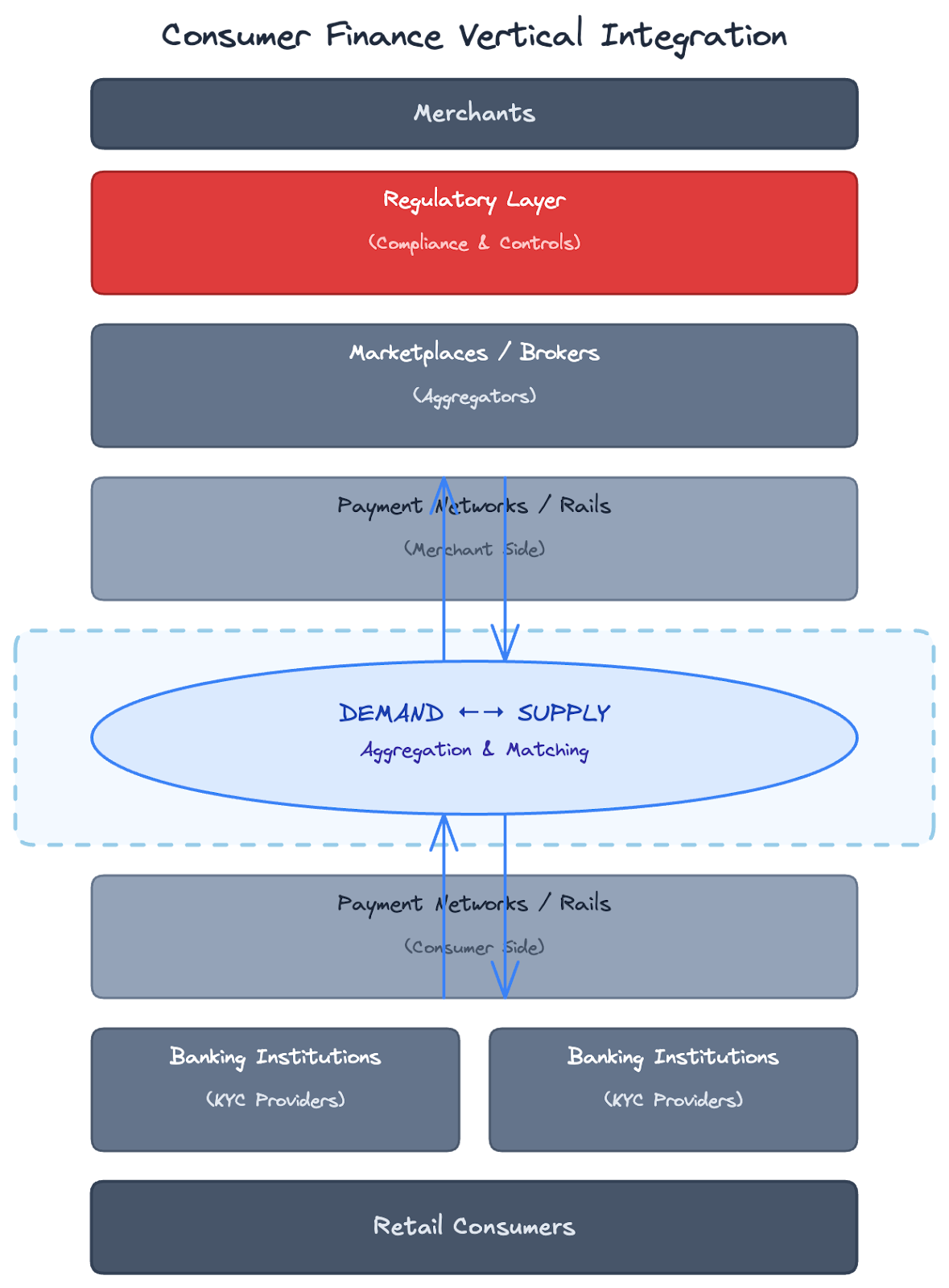

But in consumer finance, the bundling happens in cascading waves. Start at the bottom with raw demand – individual users seeking financial services. Watch how the system immediately begins its aggregation dance. First come the regulatory clusters: KYC requirements that sort users into neat, compliant packages. Then the institutional layer emerges, as banks and EMIs scoop up these pre-sorted groups, adding their own wrapper of services and protections.

The magic happens as you climb higher. Each layer doesn't just aggregate – it transforms. Those localized banking relationships get swept into the grand orchestration of payment rails. They don't just bundle; they create meta-networks where the bundles themselves become commodities. It's aggregation eating itself, layer by magnificent layer.

Now flip the telescope. From the merchant side, the same forces work in reverse. Individual suppliers get corralled first by compliance – export controls, service regulations, the whole bureaucratic apparatus. Then come the marketplaces and brokers, aggregating not just for efficiency but for power. By the time these supply chains reach the payment layer, they've been so thoroughly bundled that the original merchants are barely recognizable.

Though subtly different in how they arrive at the mirror in the middle, the buckets of supply and demand that sit either side of each other within the vertical have layers that definitely rhyme.

The Inert Mirror

While not completely static, this center ground has significant inertia in wholesale matching of uniquely new buckets from one side of the vertical to the other.

The mirror resists change through three interlocking mechanisms, each more insidious than the last. First comes the technical cost of switching – but this isn't about APIs or integration complexity. It's about unwinding operational muscle memory. Merchants haven't just integrated payment rails; they've embedded them into their operations, creating an infrastructure inertia so powerful that superior solutions routinely fail. The genius of stablecoin disruption reveals the only way to beat this: make switching irrelevant by creating parallel infrastructure for new use cases rather than replacements. Sometimes the best way to beat switching costs is to render them moot.

The second lock is more elegant: regulatory fear. KYC providers discovered that switching isn't technically hard – it's the compliance officer's cold sweat at explaining new vendors to regulators. This isn't switching cost; it's switching terror. Institutions cling to providers who've passed regulatory muster, creating a moat built on bureaucratic anxiety rather than technical superiority. Incumbents don't need to be best; just least likely to trigger an audit.

The third and most deceptive lock is data accumulation, which creates dependencies that grow like digital quicksand. Square builds financial biographies that become increasingly valuable, creating switching costs measured in lost context. Yet the cruel irony: data moats are fragile. EMI players sit on transaction treasures but find shallow moats because users maintain multiple relationships easily. Data only creates lock-in when it becomes irreplaceable utility. Winners transform data into indispensable insight – switching costs measured in competitive advantage, not gigabytes.

AI-Induced Dynamics

We live in a world of increasingly commoditized AI now, and the sheer pace and scale upon which it has arrived has thrown everything back into first principles thinking.

This commoditization creates a cascade effect throughout the entire tech stack. The cost of development is rapidly trending toward zero, taking with it those intrinsic moats that once protected incumbent players. What used to require teams of PhDs and years of R&D can now be spun up by any well-enabled product team over a long weekend. Anything short of deep tech or protected insider knowledge has become fair game. We've demonstrated this thesis repeatedly in our own work.

The same democratization has come for data itself. Outside the fortress-like repositories of Google and Meta, data has become surprisingly accessible to anyone determined enough to acquire it. The portability that was once a bug is now a feature, eroding another traditional source of competitive advantage.

Yet the old order persists, if in altered form. Regulatory complexity, risk management requirements, and capital intensity create new types of moats even as the technical ones crumble. Players large and small adapt, each finding their own unique flavor of network effects in this new landscape. The game hasn't ended – it's simply evolved.

Orchestrators as Brokers

There will never be a single player that sits up and down the entire vertical, and certainly not anything that might resemble a monopolistic one.

Outside of the fact it's a regulatory non-starter, even if you were just to service the West, the sheer capital and associated governance necessary to become such a behemoth is herculean. Not to mention the aforementioned rapidly eroding tech and product moats most of the incumbents already have; niche and diversified players would easily be able to eat away at any kind of serious attempt to wholly own the whole vertical.

That said, I am intrigued by the idea of what a truly universal Orchestrator service would look like – one that can span the entire vertical, touching the myriad of groups, aggregations, and buckets of supply and demand, and seamlessly facilitate their interaction with each other.

On the user demand side: automatic provisioning of accounts and the handling of associated paperwork and process that comes with that. Guaranteeing execution finality on the supply they want to access, with just-in-time creation of the glue – the financial rails – that still behave in the ways they're used to.

Supply would be faced with the single largest centralized pool of liquidity and customers possible, free from the burden of needing to understand and manage the various mechanisms that led to them getting paid, nor the maze of regulatory and consumer protection requirements they're beholden to, with the orchestrator alleviating them of that burden by design of it acting akin to a broker.

The Coalescence of Two Worlds

Just as the commoditization of AI and its subsequent Agents begins to really scale knowledge work to the point where it can become truly democratized, stablecoin-based settlement rails and the continued march towards asset tokenization has presented consumers with a Cambrian explosion of FinTech services to secure their financial freedom.

Never before has there been this many disparate groups of supply and demand, all eating away at traditional players and their network effects, whilst simultaneously fragmenting liquidity in the market. A perfectly timed convergence of two of the largest – and at least in recent years – most impactful tech sectors to potentially enable something radical.

The New Paradigm

This isn't the death of network effects, but their evolution. Traditional network effects created winner-take-all dynamics through user lock-in. Orchestration effects; where value accrues not from trapping users, but from reducing friction across the entire ecosystem.

The next generation of winners won't be those who build the highest walls around their users, but those who tear down walls between services, creating value through connection rather than capture.